In the Shadow of Superpowers: Implications of Europe’s Increased Defense Spending in NATO

Executive Summary

Since the start of the Russian invasion of Ukraine in February 2022, the NATO alliance has been reminded of its main objective: to counterweight Russian (Soviet) threats in central and eastern Europe. NATO’s changing status from a post-Cold War peace project to a hard-power alliance comes at the risk of securing peace through strength, especially for European NATO members. The alliance, once led by the United States (US), now faces an American withdrawal of funding and long-term commitment. With the retracted US role, Europe will have to take the burden of collective security and defense across the continent.

The changing nature of the world order compels Europe to undertake a fundamental reassessment of long-held assumptions and defense priorities as the rules-based system fades in the shadow of superpowers. Europe’s pledge to increase defense spending by 5% by 2035 within the NATO alliance is complemented by its European Defense Readiness 2030 initiative, also called re-arming Europe. Although increased defense spending is an absolute necessity to counter future threats from adversaries, mainly Russia, it also risks militarizing Europe while strategically bolstering deterrence.

This brief analysis examines the following central question: will increased defense spending by European countries in NATO risk militarizing the continent while bolstering deterrence? Particularly, how does higher defense spending benefit/impact Eastern Europe, namely the Baltic states, Poland, Ukraine, Romania, and Bulgaria?

Europe faces multiple perceived challenges as defense spending increases, including fiscal pressure, an underdeveloped industrial base, technological integration, a shortage of skilled labor, access to critical minerals and supply chains, interoperability, and overall battlefield readiness. To gain a strategic military edge, these shortfalls must be overcome as the continent braces for a confluence of direct military threats, systemic geopolitical competition, and a changing international alliance system.

The push for increased defense spending raises significant militarization risks. As European nations ramp up their military capabilities, there is a danger of entering a security dilemma, where defensive postures are perceived as aggressive by adversaries, potentially leading to arms races and miscalculations. Historical precedents, such as the pre-World War I and World War II arms buildups, illustrate how rapid militarization can undermine diplomatic solutions and escalate tensions. The current trajectory of NATO's militarization, particularly along its eastern flank, risks validating Russian narratives of encirclement and aggression, further complicating the security landscape.

Moreover, the focus on military expenditure does not guarantee enhanced combat capabilities. The confusion between input (spending) and output (military effectiveness) poses a critical challenge, as increased budgets must translate into tangible military power. This necessitates overcoming structural issues within European defense industries, such as fragmentation and reliance on US technology, military mass, and firepower, to ensure that increased spending leads to improved operational readiness and deterrence capabilities.

In conclusion, while Europe's commitment to bolster its defense spending is a necessary response to contemporary threats, it must be approached with caution to avoid the pitfalls of militarization that could destabilize the region further. The challenge lies in balancing the need for enhanced military capabilities with the imperative of maintaining diplomatic avenues for conflict resolution.

We live in a world in which you can talk all you want about international niceties and everything else, but we live in a world—in the real world, Jake—that is governed by strength, that is governed by force, that is governed by power. These are the iron laws of the world that have existed since the beginning of time

Stephen Miller, US Deputy Chief of Staff for policy and homeland security advisor.

Europe, NATO, and the Iron Laws of the World

The North Atlantic Treaty Organization (NATO), since its founding in 1949, has been a key player in Europe’s defense and security. While the NATO alliance remains a cornerstone of collective defense, it faces fundamental challenges as the international order undergoes changes of a magnitude not seen since 1945. Equally important are the old assumptions of the post-Cold War era, where the implicit guarantee of US military power allowed for defense underinvestment by European nations. Such security guarantees are off the table as current remarks of US disengagement, coupled with direct threats from Russia and China's growing economic domination, propel European nations to ramp up defense spending across the continent. When the iron laws of the world are at play, sheer military power and strength become the defining imperative for increased deterrence. This new reality compels European nations to relearn the vocabulary of deterrence, defense industrial capacity, and battlefield readiness; in other words, peace through strength.

The NATO alliance has provided the formidable platform for Europe to pursue collective security. The alliance set spending targets at two percent of GDP for all member states at the 2014 summit. However, most NATO members spent less than the required two percent, while the US took the lion’s share of the alliance’s defense spending. Donald Trump’s second term swiftly transformed both NATO and European security infrastructure and demanded all NATO members spend a minimum of two percent of their GDP and embrace a burden-sharing policy. Based on 2024 estimates, eight European NATO members are currently spending under two percent of GDP: Croatia (1.9%), Montenegro (1.7%), Italy (1.5%), Portugal (1.5%), Slovenia (1.4%), Luxembourg (1.3%), Belgium (1.3%), and Spain (1.2%).1 The US’s break from automatic US intervention and security umbrella for Europe has injected a sense of urgency into European members of NATO who are not only committed to spending 2 percent on defense but also pledge to spend a staggering 5 percent by 2035. Of course, this pledge excludes Spain, who “will not meet the 5% defense spending goal, calling the two percent target 'sufficient' and 'realistic' for the country,"2 stated Spain’s Prime Minister Pedro Sánchez in NATO’s June Summit in The Hague, 2025.

Achieving this objective requires European nations to abandon peacetime complacency and shift to a “wartime mindset” to confront the reality of high-intensity war, as stated by Mark Rute, NATO Secretary General, during the NATO Summit in June 2025. A wartime mindset places Europe on a war footing that requires substantial reevaluation of defense spending and industrial capability. The 5% defense investment commitment by 20353 demonstrates a credible commitment by European members of NATO to shoulder a greater share of the financial burden. It also sends a political signal to the world that European rearmament is a strategic necessity to “restore credible deterrence and deliver the security on which our [Europe’s] prosperity depends,” as outlined in the White Paper for European Defense Readiness 2030.4

The main question is whether higher defense spending leads to a militarized Europe for the coming decades. Particularly, it is significant to understand how higher defense spending will impact Eastern Europe, namely the Baltic states, Poland, Ukraine, Romania, and Bulgaria. The paper explores the risk of militarization in Europe as defense spending in NATO reaches 5% by 2035. It also addresses the centrality of increased deterrence through defense spending and weighs it against acquiring real military readiness.

The White Paper for European Defense Readiness 2030 outlines Europe’s growing threats and security challenges in its region and beyond:

“Strategic competition is increasing in our wider neighborhood, from the Arctic to the Baltic to the Middle East and North Africa. Transnational challenges such as rapid technological change, migration, and climate change could put immense stress upon our political and economic system. Authoritarian states like China increasingly seek to assert their authority and control in our economy and society. Traditional allies and partners, such as the United States, are also changing their focus away from Europe to other regions of the world.”

The moment has come for Europe to rearm, and with it the end of Europe’s peacetime vision of security built on “arms control, transparency, and confidence-building mechanisms (CBMs)," which was once heralded as the cornerstone of European security. This shift away from the principles laid out in the 1990 Treaty on Conventional Armed Forces in Europe (CFE)5 has significant implications for Europe and the world. In a world where security is viewed through the lens of hard power and deterrence, a more militarized posture may risk diplomatic disengagement. This is especially true for Europe; given the pretext of two World Wars on the continent, the risk of militarization may undermine current and future efforts towards meaningful peace and dialogue. One thing is clear, and that is that New Europe, based on confidence- and security-building measures,6 is reduced to a mere theory.

Above all, Europe’s shift to hard power and forward deterrence faces multiple perceived challenges as defense spending increases, including fiscal pressure, an underdeveloped industrial base, technological integration, a shortage of skilled labor, access to critical minerals and supply chains, interoperability, and overall battlefield readiness. To gain a strategic military edge, these shortfalls must be overcome as the continent braces for a confluence of direct military threats, systemic geopolitical competition, and a changing international alliance system. Nonetheless, Europe’s commitment to spend 5% of GDP in NATO comes from both historical memory of war and an acute awareness of contemporary threats across and beyond the continent. Perhaps Europe’s policy to carve out a place for itself in the global race toward military modernization and technological and economic advantage is best reflected in Mark Rutte’s remarks on the future of Europe and the NATO alliance: “To Prevent War, NATO must spend more.”7

Theoretical Framework

The art of war has been developing and undergoing substantial transformations since ancient times that have principally aimed at ensuring the security of the state. This analysis draws on classical realist theory, which contends that states prioritize military power for survival in an anarchic international system. Russia’s 9 percent GDP war economy and China’s near-complete dominance of rare earths (REs) demand European NATO members’ 5 percent spending pledge as the most realist approach and principle of peace through strength.

Professor John Mearsheimer's offensive realism8 illustrates why NATO’s eastern flank, also Eastern Europe, such as Poland at 4.2 percent GDP and the Baltics above 3 percent, surges ahead in defense spending. The return of geopolitical competition and their proximity to Russian threats compels power maximization, even at the risk of regional arms races.9 Equally important is the fundamental decades-long challenge between the West and Russia over the expansion of NATO. The relentless expansion of NATO, framed by Mearsheimer in abstract power-political terms, is seen from the outside as the military consolidation of a metropolitan core (led through a capitalist lens and justified as collective national interests), extending its security umbrella to lock in the gains of the post-Cold War expansion and strategically pen in rivals like Russia.10 In this sense, NATO’s expansion provokes a Russian security dilemma, just as much as Russia’s ”natural“ great power security needs trigger a mutual dilemma for the West.

Alliance burden-sharing theory from Mancur Olson and Richard Zeckhauser11 illuminates transatlantic imbalances. For instance, NATO’s spending benchmark since 2014 has not been met by many European country members, where the United States historically over-contributes with $967 billion against Europe's $343 billion, enabling free-riding by laggards like Italy at 1.5% and Spain at 1.2%. With Europe’s increased spending threshold, equitable contributions to NATO will be met; however, foundational capability gaps in missile defense and Intelligence, Surveillance, and Reconnaissance (ISR) reveal that spending alone does not guarantee readiness.

Another important aspect to explore is the link between increasing defense capabilities and militarization risks. Robert Jervis's “Cooperation under the Security Dilemma”12 frames the militarization risks and applies the concept of “all chase rabbits,” where the order of preference is arms competition and high risk of war. Europe's race to rearm the continent through gradual abandonment of the Conventional Armed Forces in Europe (CFE) treaty increases deterrence against Russia and adversaries but also risks escalation through miscalculation. Mark Rutte’s remarks on the shift to a ”wartime mindset” strengthen credibility across Europe, particularly on the eastern flank. Yet, such a wartime mindset echoes pre-World War I dynamics, where arms buildups undermined diplomatic solutions, as explained in Jervis’s security dilemma.13 NATO Watch analysis (2030)14 warns that accelerated spending risks nuclear escalation and diplomatic isolation.

Together, these theoretical frameworks explain Europe’s rearmament and NATO’s evolution from a post-Cold War peace project to a hard-power alliance. In the post-Cold War order, the alliance and Europe’s success heavily depend on transforming financial inputs into operational outputs like interoperability and ammunition stockpiles. Burden-sharing collapse risks are minimal at the moment, despite the United States’ pivot from Europe and specific ambitions of acquiring Greenland. It is important, though, to see how the 2025 US National Security Strategy's reduced focus on European priorities impacts the NATO alliance and what Europe’s increased spending means for the coming decade.

The growing multipolarity of the international system is carving the world into spheres of influence, mostly between the US, Russia, and China.

Deconstructing Threats to European Security

A range of interconnected security threats shape Europe’s strategic context, as explained in the White Paper for European Defense Readiness 2030. From a geopolitical standpoint, Europe’s geography and history make it vulnerable to certain security challenges in the wider European neighborhood. Specifically, proximity to North Africa and the Middle East makes Europe a receptacle for the spillover of the wars emanating from the region. These threats also include migration waves and effects of climate change that have afflicted the MENA region. To the north, the Arctic is becoming a highly geostrategic location, of which increasing geopolitical competition will directly influence Europe’s security. In the Western Hemisphere, particularly the Atlantic, the changing position of the US from a traditional ally to a skeptic that claims overcommitment to Europe and is in need of rebalance is clear. The US National Strategy 2025 also depicts a shift from Europe, thus reducing the US's historical role as a primary security guarantor. Non-conventional security threats such as terrorism and violent extremism, hybrid attacks, and the actions of international organized crime groups and networks of cybercriminals are increasing in prevalence across continental Europe. The growing connection between these hostile groups enabled by new technologies poses unconventional security threats to Europe, which easily transcend borders.

The growing multipolarity of the international system is carving the world into spheres of influence, mostly between the US, Russia, and China. Europe, while still catching up in an increasing systemic competition, needs to build up sufficient deterrence capacity not only to deter a future war of aggression but also to strategically compete in the global race for technological innovation and military domination. In today’s hyper-competitive and transactional geopolitics, the three highest-priority threats to address include:

First: Direct Military Threat from Russia

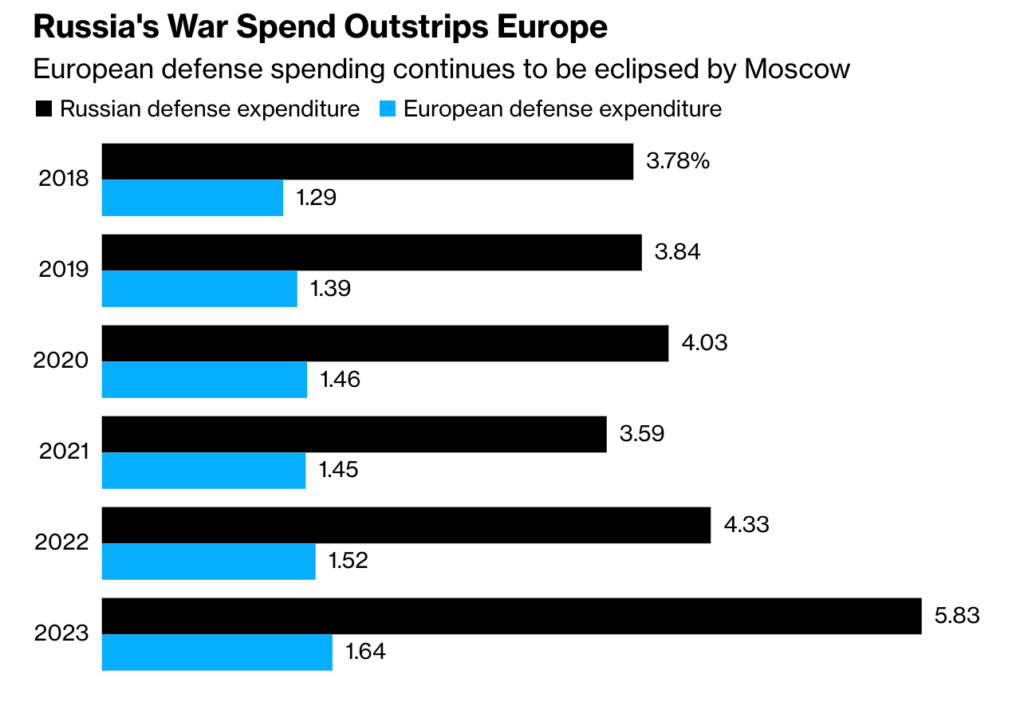

Russia remains a fundamental security threat to European security for the foreseeable future. Supported by Belarus, North Korea, and Iran, Russia’s military-industrial production capacity continues to grow with an estimated spending of 40% of the Russian federal budget in 2024, which is 9% of GDP. Russia's draft federal budget for 2024-2027 mainly focuses on increasing and strengthening defense capacity and assumes 6.3% of GDP spending for 2025. Although Russian President Vladimir Putin stated that “We cannot increase this expenditure endlessly, because all components of the country’s life, such as the economy, the social sphere in the broadest sense of the word, science, education, and healthcare have to develop, too,” the country’s understanding is that it remains at war with the West, and thus decreasing defense expenditure is unforeseeable. Most critically, Russia’s massive defense spending outstrips Europe as depicted in Figure 3, and thus Europe’s 5% of GDP spending in NATO will be a strategic step towards safeguarding European security and battlefield readiness. Russia poses critical threats in two primary forms:

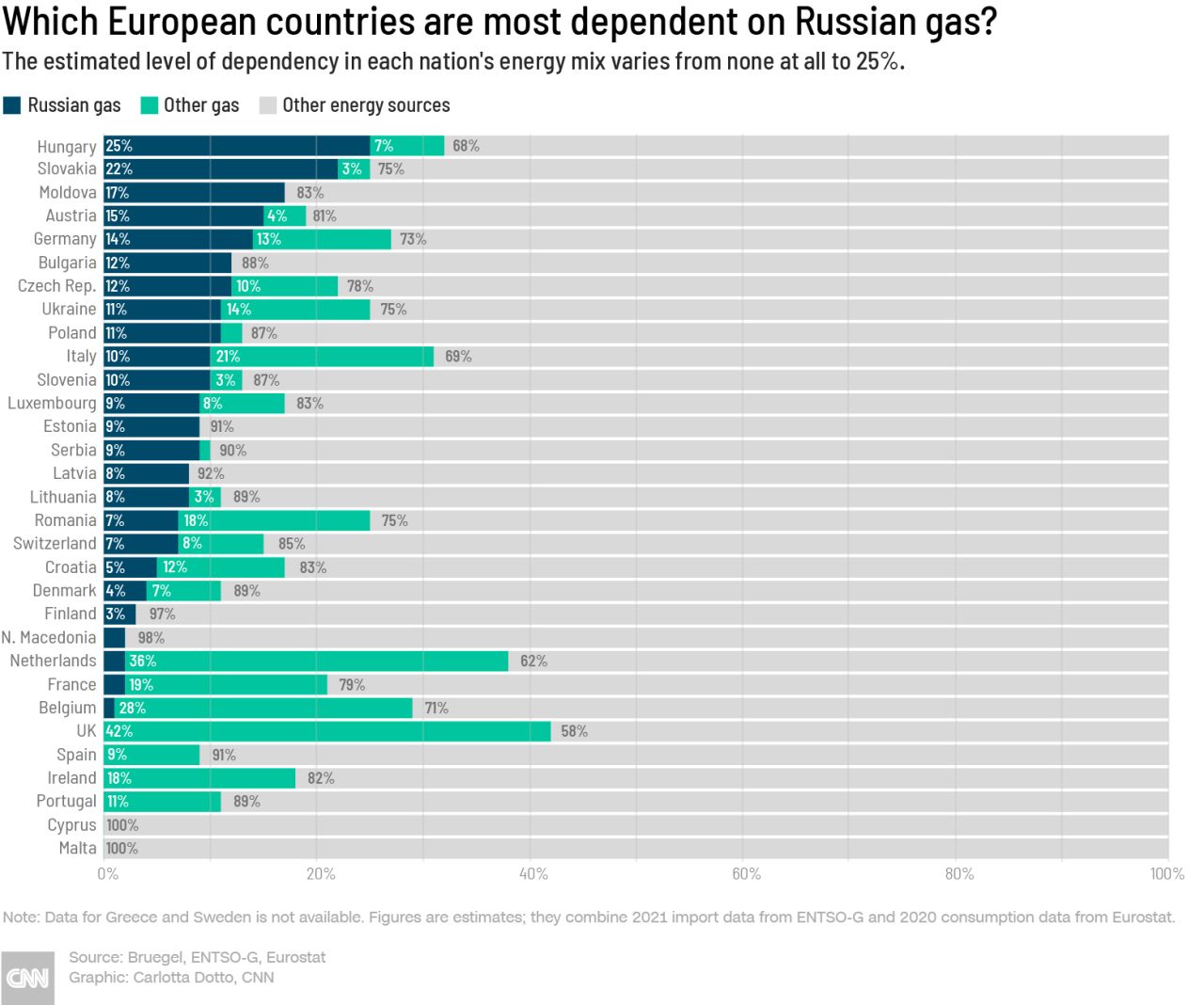

In 2021, the EU imported more than 40% of its total gas consumption, 27% of oil imports, and 46% of coal imports from Russia.

Energy security threats: Historically, the Crimean invasion in 2014 and later Russia’s war on Ukraine in 2022 marked a shift in Russia’s foreign policy and by far the return of geopolitics to the European neighborhood. Russia and Europe, particularly the institution of the European Union, enjoyed specific cordial relations with Russia, such as the EU-Russia energy relations. The energy deal has been the long-term economic cornerstone of EU-Russia relations and arguably its most strategic component.15 Before Russia’s full-scale invasion of Ukraine, the UK and EU imported a significant amount of Russian gas, as indicated in Graph 1 below. In 2021, the EU imported more than 40% of its total gas consumption, 27% of oil imports, and 46% of coal imports from Russia. Energy represented 62% of total EU imports from Russia and cost €99 billion.16 Although the EU commission announced a roadmap to fully end the EU's dependency on Russian energy, some of the largest importers of Russian fossil fuels include Hungary, France, Slovakia, Belgium, and Spain as of July 2025. Currently, European nations within the EU dropped Russian fossil fuel (oil and gas) imports by 86% between the first quarters of 2022 and 2025.17

European nations are bracing for a potential direct Russian military threat to a NATO ally in between two and five years.

Destabilizing Europe: Russia’s war objectives in Ukraine and the positioning of nuclear arsenals in Belarus constitute a direct military threat to European security. European nations are bracing for a potential direct Russian military threat to a NATO ally in between two and five years, which is explicitly described as a short window for defense planning and capability development. Other forms of Russian threats constitute less conventional military power that directly destabilizes Europe, including a coordinated hybrid warfare, also described as a shadow war against the West. The White Paper identifies the Western Balkans, Georgia, Moldova, or Armenia as areas under Russian threats. Europe’s eastern flank, namely the Baltics (Estonia, Latvia, and Lithuania), Poland, Romania, and Bulgaria, remains Europe’s and NATO’s frontlines as the Ukraine war steps into its fifth year in February 2026. Particularly, hybrid warfare18 is taking prevalence as one of Russia’s indirect threats towards European security, and they include:19

- Information and influence operations encompass psychological operations and propaganda.

- Offensive cyber operations and electronic warfare.

- Support to state and non-state partners such as guerrillas and proxy forces.

- Covert and clandestine actions by intelligence and special operations forces, including sabotage and subversion.

- Economic coercion

The EU-China relationship can be broadly classified as a systemic, economic rivalry and, in some areas, a cooperative partnership.

Second: Systemic Rivalry from China

The rise of China has profound security implications for Europe. First, China’s approach to trade, investment, and technology seeks primacy and, in some cases, supremacy. Although China remains a key trading partner for the EU, its ever-expanding ambitions threaten Europe’s import reliability, industrial competitiveness, and also defense, given China’s control over critical raw materials, also called rare earths (REs). After the US, China now has the second-highest military spending in the world, surpassing all other Asian countries combined.20 The Pentagon’s 2025 China Military Power Report refers to a dramatic expansion of China’s stockpile, which is primarily being prompted by the large-scale development and modernization of China’s next-generation intercontinental ballistic missile (ICBM) forces. Additionally, many of these missile types will be capable of carrying multiple warheads.21 The EU-China relationship can be broadly classified as a systemic, economic rivalry and, in some areas, a cooperative partnership.22 China’s backing of Moscow’s war efforts, coupled with strategic control over global rare earth supplies, poses security and economic threats to Europe.

Resource security: Europe almost entirely depends on China for nearly all rare earth minerals, which encompass 17 chemically similar metallic elements that serve as the foundation for modern technological civilization.23 The European Union alone imports approximately 85-90% of its rare earth materials from Chinese suppliers. While the name alludes to the rarity of the materials, in reality they are not scarce, though their extraction and processing require sophisticated industrial capabilities that fewer nations have developed compared to China. The Western retreat from rare earth processing has led to jeopardizing the development of critical applications across Europe, including:24

- Electric vehicle motors and battery systems

- Wind turbine generators for renewable energy

- Smartphone components and semiconductor manufacturing

- Military defense systems and advanced weaponry

- Medical imaging equipment, including MRI machines

- Industrial automation and robotics systems

At the moment, China controls 70% of global rare earth oxide output while commanding an estimated 85–90% of the global processing capacity.

Europe’s strategic weakness appeared when China’s 2025 export controls on rare earths denied licenses to defense-linked firms across Europe. The export controls require end-user certificates/licenses for dual-use exports to Europe,25 explicitly prohibiting military/defense end-uses, such as ammunition, missiles, and radar. Europe’s current rare earth crisis was triggered by the Netherlands when it placed Chinese-owned semiconductor company Nexperia26 under government surveillance in 2025. This action, although taken as a measure of national security regarding Chinese control over critical semiconductor infrastructure, quickly escalated and prompted China to implement targeted export controls on rare earths going to European markets. The sectors that are most affected by supply disruption are automotive, renewable energy, electronics, defense, and medical technology. Also, China’s rare earth dominance will have profound effects on defense modernization programs across NATO and Quad nations cooperation frameworks (United States, Japan, Australia, and India), which increasingly focus on rare earth supply chain coordination.27 As such, resource security28 is becoming an essential imperative for broader European security and beyond. At the moment, China controls 70% of global rare earth oxide output while commanding an estimated 85–90% of the global processing capacity.29 Historically, the US once led the world’s largest rare earth production, mainly from California. From the 1990s onward, Western rare earth facilities, such as US Mountain Pass and Australian Lynas, operated with strict environmental regulations, significantly increasing costs and leading to closure. Meanwhile, Chinese counterparts30 operated with minimal environmental rules, enabling low-cost, high-value production and leading to China‘s supremacy in 2010. The following chart/graph shows China’s historical production growth data from 1990 to 2025:

| Year | China Share | US Share | Shifts in production |

| 1990 | 27% | 33% | US-led global production |

| 2000 | 73% | 8% | China's rapid dominance begins |

| 2010 | 97% | ~0% | US production effectively ceased |

| 2025 | 85-90% | Minimal | China retains refining monopoly despite diversification |

Geopolitical risks: While becoming more hostile to Europe, China enjoys bilateral relations with Russia31 and has deepened cooperation in energy, trade, security, and technology sectors. Besides investing in technologies, such as AI, quantum computing, and space capabilities, China is expanding its nuclear arsenal dramatically. Current projections suggest China could possess over 1,000 nuclear warheads by 2030.32 Concerns peak over China’s actions in the East and South China Sea, in addition to Taiwan. Existing military, political, economic, cyber, and cognitive measures aimed at coercing Taiwan raise the risk of a major disruption with profound economic and strategic consequences for Europe, as explained in the European Defense Readiness 2030. These mounting external threats from China and Russia are heightened by a fundamental re-evaluation of the transatlantic relationship with the US, which has long served as the bedrock of European defense and security architecture.

Arguably, the US’s radical shift in foreign policy priorities serves as the driving factor in European defense architecture for the coming decade.

Third: Re-Assessing the US Role

One cannot separate Europe's increased defense spending in NATO from the fundamental shift in the transatlantic relationship with the US. Europe’s increasing appetite for autonomy and its responsibility to defend the continent reflect a long-term rebalancing act by the US under Trump’s second administration, which has shifted its foreign policy direction towards the Indo-Pacific and its orbit of influence, the Western Hemisphere. With the US focusing on Greenland, European countries are acknowledging that a future US administration could disengage from the NATO alliance. Arguably, the US’s radical shift in foreign policy priorities serves as the driving factor in European defense architecture for the coming decade.

Points of Contention: Although the US remains anchored to the NATO alliance, its latest foreign policy intentions toward taking Greenland33 could be the splintering of the alliance itself. The US rationale for annexing Greenland highlights the fundamental geopolitical presence of Russia and China in the Arctic region,34 making it a national security imperative for the United States. Beyond Greenland, the US National Security Strategy (NSS, 2025) significantly de-emphasizes China’s existential threat,35 which is less alarmist compared to the European Defense Readiness (2030)’s view of China as a “systemic rival.”

The pressure to secure peace in Ukraine markedly impacts the transatlantic alliance, especially when Europe can no longer assume the US will automatically underwrite its security in a similar crisis.

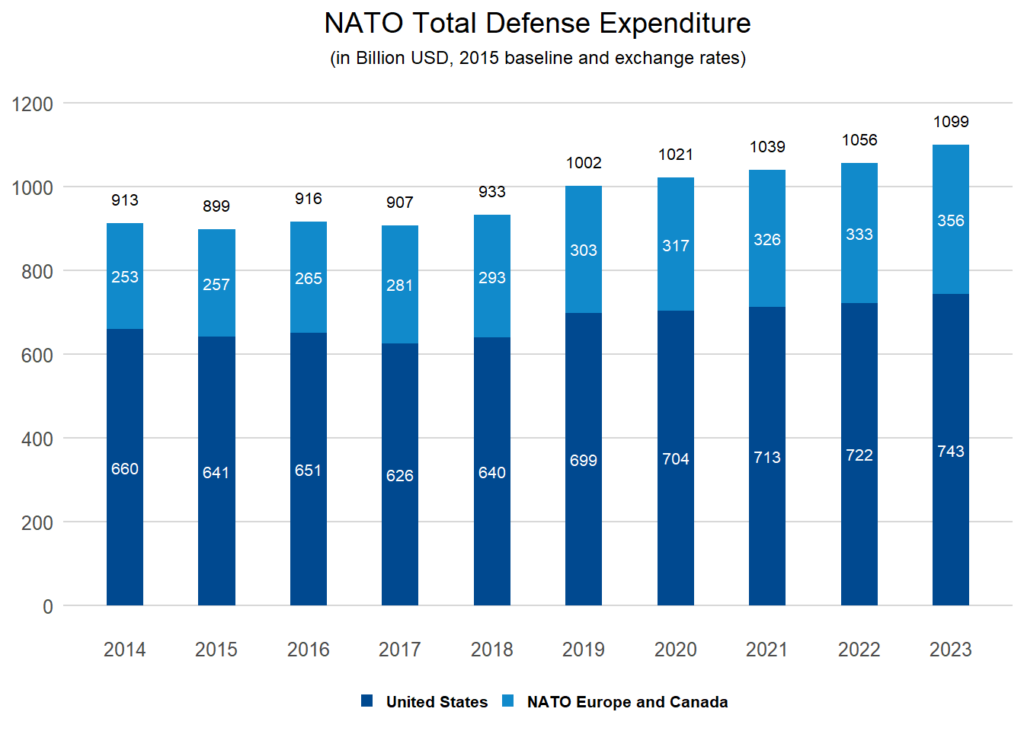

US diplomatic talks to end the Ukraine war add further contention, given its proposed 20-point peace plan. The plan advocates a "free economic zone” in Donbas if Ukraine cedes the Donbas region while creating a “demilitarized zone“36 in the Donetsk region. Ukraine has swiftly rejected ceding lands, in addition to European countries favoring prolonged war over territorial compromises. The pressure to secure peace in Ukraine markedly impacts the transatlantic alliance, especially when Europe can no longer assume the US will automatically underwrite its security in a similar crisis. US trade tariff impositions on European countries increase the likelihood of a transatlantic rift37 and a break from the old alliance system in the post-Cold War era. Besides, there are defense spending imbalances between the US and Europe in the transatlantic alliance. NATO’s total defense spending between 2014 and 2023, depicted below, reveals America’s massive defense spending in NATO, reaching $967 billion (3.38% GDP),38 far exceeding Europe and Canada combined at nearly $507 billion and Europe alone at $343B (EU27).39 NATO’s new spending benchmark at 5% of GDP signals Europe’s readiness to shoulder the burden of defense and security, primarily as a deterrent to NATO’s adversaries, foremost among them Russia.

The reality of a fragmented European defense manifests in defense funding differences and uneven modernization paces, which directly undermine the operational cohesion of the NATO alliance.

Analysis of Defense Spending, Capabilities, and Gaps

At the heart of the NATO alliance lies a simple equation: Capability x Will = Deterrence. Combined with a “wartime mindset,” Europe's defense architecture under NATO’s deterrence as a defense approach40 profoundly moves away from peacetime military and security buildups to rapid, high-volume production. Accelerating the growth of defense industrial capacity and production in this sense highly depends on a shift in military culture driven by constant readiness and not cyclical readiness.41 The burden-sharing imperative42 among European NATO members remains a key factor in producing this change. However, divergence in commitment to this trend among European countries has led to the creation of what some scholars refer to as an emerging “Multi-Track NATO.”43 The reality of a fragmented European defense manifests in defense funding differences and uneven modernization paces,44 which directly undermine the operational cohesion of the NATO alliance. Moreover, this divergence has led to different categories of performers, with the eastern flank leading in the category of Star Performers.

The Star Performers

Eastern flank states, namely Poland, the Baltics, Romania, and Bulgaria, driven by direct military threats from Russia, surge ahead with wartime resolve and exceed spending targets. These nations are not only star performers in defense spending but also are at the forefront of NATO’s forward deterrence. For Europe, the eastern flank is vital in relearning deterrence and raising the nuclear IQ45 as foundational imperatives to securing peace:46

Poland and the Baltics: at 4.2 percent of GDP, Poland leads the Star Performers’ cohort, fielding 250 HIMARS launchers for deep strikes, 48 FA-50 light combat jets, and a territorial defense force training 400,000 civilians for hybrid resistance.47 Despite modest economies, the Baltic states have tripled expenditures since 2014, as indicated below: Estonia (3.4 percent), Latvia (3.1 percent), and Lithuania (3.2 percent). The Baltics are actively integrating NASAMS medium-range air defenses, brigade-sized rotations, and e-mobility for rapid reinforcement.

Romania and Bulgaria: as frontline performers, both are spending 2.5 two and a half percent and two percent, respectively. Romania and Bulgaria are emerging beyond buffer states and will soon be shouldering NATO and Europe’s forward deterrence efforts in bolstering Black Sea deterrence against Russian Kalibr threats.

| Rank | Country | Increase Since 2014 | 2024% GDP |

| 1 | Poland | +300% (now NATO leader at 4.7%) | 4.12% |

| 2 | Lithuania | +250% (tripled spending) | 3.2% |

| 3 | Latvia | +230% (tripled spending) | 3.1% |

| 4 | Germany | +89% (€90.6B absolute leader) | 2.12% |

| 5 | Estonia | +200% | 3.4% |

| 6 | Romania | +190% | 2.5% |

| 7 | Finland | +180% (post-NATO join) | 2.6% |

| 8 | Sweden | +150% (doubled spending) | 2.2% |

The Aspirational Committers

While this group consists mostly of larger European economies, they face structural financial and capability hurdles in translating defense commitments into tangible military capability. Germany, the United Kingdom (UK), France, Sweden, and Finland fall under the category of aspirational powers with landmark spending pledges while dealing with systemic underinvestment legacies:

Germany invests €100 billion in the Zeitenwende special fund,49 directed at accelerating Arrow-3 exo-atmospheric interceptors and Heron TP armed drones.50 Bureaucratic hurdles and procurement delays have slowed Germany's defense plans, limiting 2026 spending to 2.1 percent of GDP, with only partial F-35 integration.

The United Kingdom recently committed to spending 2.5 percent,51 albeit with a backlog that will only become available from 2027 onward. Currently, the UK channels funds into Tempest GCAP sixth-generation fighters and Type-26 frigates for global power projection, though industrial ramp-up strains shipyard capacity.

France maintains a steady 2.1 percent investment52 in Rafale upgrades, ASN4G hypersonic air-launched missiles, and Scorpene submarines, leveraging its autonomous nuclear triad for strategic autonomy.

In the post-2023 NATO accession, Sweden is spending 2.2 percent with plans to reach 2.8 percent of GDP in 2026, rising to 3.1 percent in 2028, with a target of 3.5 percent by 2030.53 Finland’s defense spending is currently at 2.6 percent, and the Finnish government has proposed raising it to at least 3% of GDP by 2029.54 Both countries are well positioned among NATO allies and deploy Archer self-propelled howitzers and Gripen-E fighters55 while pooling troops through the Nordic Defense Cooperation (NORDEFCO) for high-north and Baltic mobility56 in the wake of Russia’s expanding presence and militarization in the Arctic.57

The Lagging Cohort

Also called “Laggards,” Italy and Spain continue to fall short of NATO’s two percent spending benchmark. The reasons for this shortfall vary from domestic opposition to increased military spending to existing fiscal pressures, in addition to fundamental differences in perception regarding nature and the immediacy of the threats facing Europe. This multi-track NATO reality reveals structural disparities between NATO’s flanks, where geography fundamentally shapes defense priorities, as evident in the cases of Italy and Spain:

Italy’s low defense spending lingers at 1.5 percent,58 with particular focus on Mediterranean stability operations over eastern flank threats.

Spain's spending is at 1.2 percent, and it has reached an agreement with NATO to allocate 2.1 percent of GDP to defense.59 However, the country deems two percent sufficient and has not agreed to 5 percent spending, as Prime Minister Pedro Sánchez affirmed at the 2025 Hague Summit.

Beyond the 7 priority areas outlined in Defense Readiness 2030, rebuilding European defense requires overcoming the obstacles facing the multi-track NATO first while ensuring defense spending leads to enhanced security and military readiness.

| Priority Area | Overview |

| Air and Missile Defense | Integrated, multilayered system protecting against the full spectrum of air threats, including cruise missiles, ballistic and hypersonic missiles, aircraft, and UAS. |

| Artillery Systems | Advanced fire systems with modern artillery and long-range missile systems for precise, deep precision strikes against land targets. |

| Ammunition and Missiles | Strategic stockpiles of ammunition, missiles, and components based on the European External Action Service "Ammunition Plan 2.0," with sufficient industrial production capacity for timely replenishment. |

| Drones and Counter-Drone Systems | Unmanned systems (aerial, ground, surface, and underwater) are controlled remotely or autonomously using advanced software and sensors for enhanced situation awareness, surveillance, and other capabilities. |

| Military Mobility | EU-wide network of land corridors, airports, seaports, and support elements facilitating seamless, rapid transport of troops and equipment across the EU and partner countries. |

| AI, Quantum, Cyber & Electronic Warfare | Defense applications leveraging military AI and quantum computing; advanced electronic systems to protect electromagnetic spectrum use, disrupt opponents, and secure cyber operations. This includes a voluntary EU scheme for offensive cyber deterrence. |

| Strategic Enablers and Critical Infrastructure Protection | Strategic airlift, air-to-air refueling, intelligence/surveillance, maritime domain awareness, space assets, secure communications, and military fuel infrastructure protection. |

Beyond securing the billions, Europe’s central challenge contains a fundamental risk: conflating annual expenditure flows with accumulated military power.

Evaluation of Defense Spending

The 2025 Hague Summit's ambitious 5 percent GDP benchmark comprises 3.5 percent for core defense requirements, such as equipment and forces, plus 1.5 percent for adjacent resilience, innovation, and critical infrastructure protection. This new spending benchmark imposes fiscal burdens and requires fiscal mobilization60 unseen since the Cold War era. The 5 percent spending remains a necessary precondition for European rearmament to match the increasing defense spending of Russia and China, along with the decreasing American stake in Europe’s defense. While projections indicate that European NATO members will increase spending to €800 billion annually by 2035, these increases alone will not suffice. The difficulty is mainly due to translating increased funding into tangible military power, such as sustained high-intensity warfighting capacity, modern equipment stocks, institutional knowledge, or battlefield readiness.

Beyond securing the billions, Europe’s central challenge contains a fundamental risk: conflating annual expenditure flows with accumulated military power. A dramatic reprioritization of military preparedness, thus, would likely require significant trade-offs with other areas of public spending and profound shifts in national fiscal policy. This type of spending proves difficult for countries with substantial national public debts, such as France (112% of GDP) and Italy (135% of GDP).

| Country | Projected 2035 Spending at 5% GDP | Comparative Public Spending (Current) |

| Germany | ~$329 billion | ~$283 billion on education |

| France | ~$221 billion | ~$225 billion on education |

| Italy | ~$158 billion | ~$126 billion on education |

The risk of “conflating input with output," as discussed by Stockholm International Peace Research Institute (SIPRI) experts, persists as military expenditure is a flow measure—an indicator of annual investment—not a direct measure of accumulated military capability. For instance, simply spending more does not automatically translate into a more effective fighting force unless it targets the existing gaps in stock of equipment, infrastructure, institutional knowledge, and combat readiness.61 Particularly, mobilizing the necessary financial resources must capture the formidable shortfalls in military hardware and industrial capacity.

Critical Capability Shortfalls

One of the key capability shortfalls relates to the European armed forces that affect their ability to conduct complex, high-intensity military operations over a sustained period. Europe also lacks an effective industrial base, which hinders the rapid acquisition of necessary assets. Current capability shortfalls render European forces ill-equipped for peer conflict, as indicated below:62

- Integrated air and missile defense remains fragmented and inadequate, with Europe fielding roughly 200 Patriot batteries against the U.S.'s 500+ and possessing zero indigenous mid-course interceptors for ballistic threats.

- Long-range precision fires are confined primarily to France and the UK's 500 SCALP/Storm Shadow munitions, dwarfed by Russia's 4,000+ Iskander reserves capable of theater-wide suppression.

- Intelligence, surveillance, and reconnaissance (ISR) deficits hamper joint operations, limiting Europe to 150 dedicated platforms versus the U.S.'s 800+; this makes Europe too dependent on RQ-4 Global Hawk feeds for geospatial awareness.

- Ammunition and strategic stockpiles stand critically depleted after Ukraine aid consumed 80 percent of reserves; current 155 mm artillery shell production idles at 1 million rounds per year against a doctrinal need for 2.5 million in sustained operations.

- Digital sovereignty is weakened by dependence on US hyperscale cloud providers, undermining data security in contested electromagnetic environments.

Industrial Systems and Dependencies: Europe has six times more defense system types than the US while suffering from a fragmented base that contains around 180 distinct weapon types compared to the US's streamlined 30, inflating acquisition costs by 20 to 30 percent and complicating logistics.

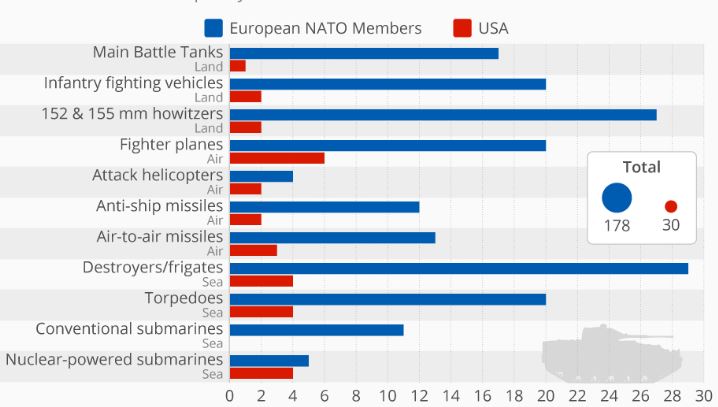

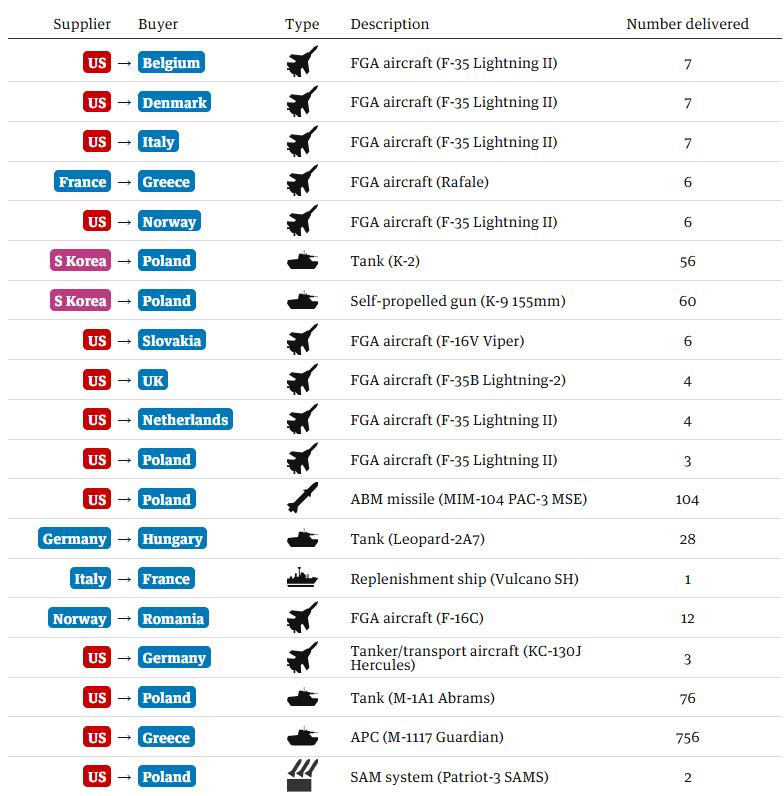

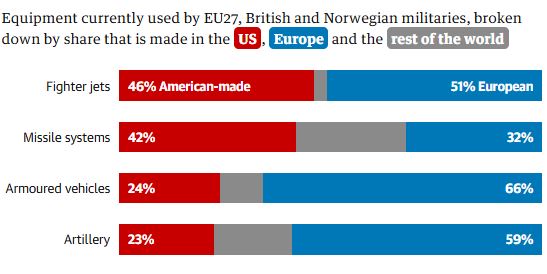

The high procurement trend from post-February 2022 reveals over $180 billion in defense contracts, with European systems gaining at least $94 billion, or 52 percent overall, according to the IISS estimates.63 These European systems are mostly strong in naval domains like frigates and submarines, while US platforms dominate aerospace markets through F-35s and high-end munitions. Nonetheless, technically, Europe's militaries depend on American hardware, in addition to the US emerging as the key arms supplier, as depicted in Figures 7 and 8.

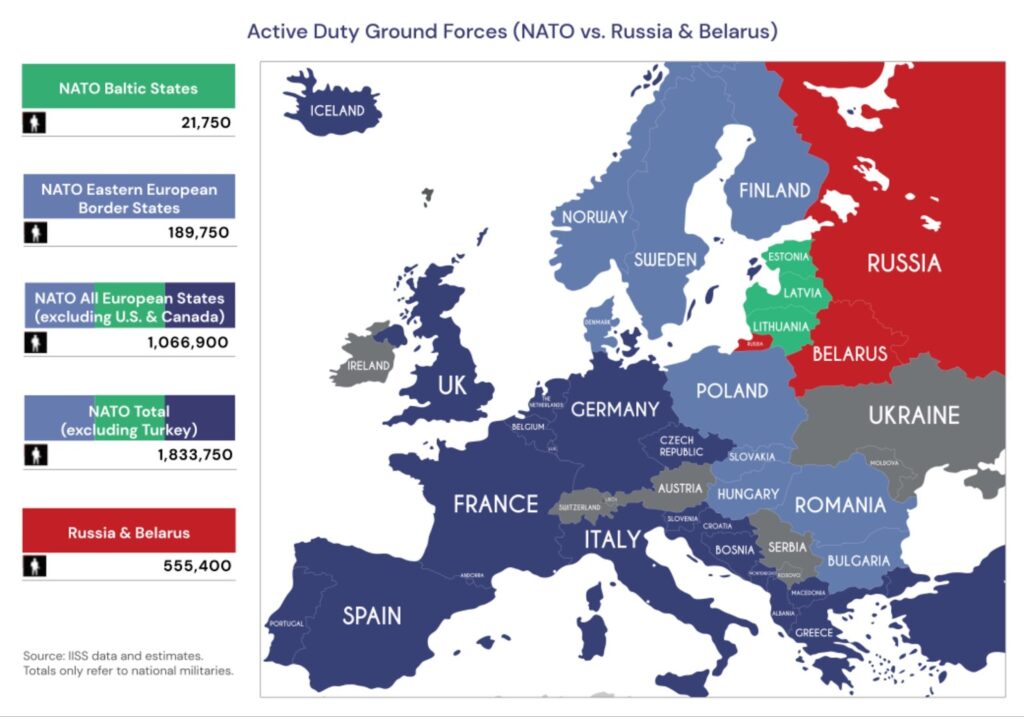

In a conflict against all European NATO countries without US involvement, Russia would currently be outnumbered 2:1 in active-duty ground forces and would face a much larger disadvantage in air and naval forces.

One of the dangers to European industrial production for 2026 onwards is China's near monopoly on rare earths (REs) processing, exacerbated by 2025 export bans. This has affected the production of EU hypersonic and glide vehicle programs, given the export controls denying magnets and a 75% drop in magnet shipments since May 202564 for defense production. Resolving these gaps requires institutionally coordinated efforts from both the European Union and the NATO alliance. Europe can leverage NATO’s principal role as the "cornerstone of collective defense"65 and thus be responsible for setting up military capability requirements, developing operative plans, and ensuring the credibility of deterrence. NATO’s geographic spread is highly important to ensuring the credibility of deterrence, especially against Russia and its ally Belarus in the eastern flank. In a conflict against all European NATO countries without US involvement, Russia would currently be outnumbered 2:1 in active-duty ground forces and would face a much larger disadvantage in air and naval forces,66 as depicted in figure 9 below.

The EU can use its own financial, regulatory, and industrial policy tools to encourage investment, cooperation, and the growth of Europe's defense technology and industrial base. The EU has launched the following suite of initiatives specifically aimed at supporting member states’ efforts to overcome the pressing challenges facing Europe:

- European Defense Fund (EDF):67 co-finances collaborative, cross-border research and development projects to foster innovation and interoperability.

- Permanent Structured Cooperation (PESCO):68 A treaty-based framework that allows willing and able EU member states to enter into more binding commitments on security and defense projects.

- European Peace Facility (EPF):69 An off-budget fund that has been instrumental in financing the provision of military equipment to Ukraine.

- The "Readiness 2030" plan (formerly ReArm Europe):70 A comprehensive framework proposed in a recent white paper to coordinate a "once-in-a-generation surge in European defense investment."

- Security and Action for Europe (SAFE) instrument:71 A proposed financial tool intended to provide up to €150 billion in loans to support member states' defense investments and common procurement.

Through the lens of the security dilemma concept, the escalation of military expenditures in Europe between pre-WWI and WWII explains that Europe’s military buildup through NATO carries the risk of being misinterpreted as offensive postures.

Weighing Militarization vs. Deterrence

One of the key outcomes of increased defense spending is militarization: the political and social transition process toward defense readiness.72 Risking a vicious security dilemma, militarization and the rise of defensive buildups significantly increase arms races, aggression, and miscalculation. Europe’s unique historical context is ripe with examples of similar security dilemmas as experienced pre-WWI/II when European countries' spending reached 3-20% GDP.73 While the shift toward a 5 percent GDP spending target is framed as a necessary evolution of deterrence, it introduces significant systemic risks regarding the militarization of the European continent. Through the lens of the security dilemma concept,74 the escalation of military expenditures in Europe75 between pre-WWI and WWII explains that Europe’s military buildup through NATO carries the risk of being misinterpreted as offensive postures. Military spending patterns pre-WWI and WWII and post-2022 (Ukraine War) below showcase a growth path in terms of overall military spending:76

Pre-WWI Militarization (1913)

Europe's arms race experienced high military burdens (military expenditures as a percentage of GDP, averaging 3–5% GDP, with Germany at 4.2%, France at 4.1%, Russia at 5.0%, and Austria-Hungary at 3.5%).77 European armies mobilized 10–12 million troops rapidly and brought the alliance tensions to the point of total war.

Pre-WWII Surge (1933-1938)

Europe’s rearmament exploded, especially that of Germany and the USSR, which peaked at 60-75% GDP by 1943-44 via total mobilization; Allies like the US/UK hit 40-50% max.78

Post-2022 (Ukraine War)

Pledge to reach 5 percent by 2035 across Europe as part of NATO (vs. 1.6-1.9% previously) totals €1T+ extra by 2035.79 This is particularly mirrored by interwar fiscal strains, where military costs may cut welfare by 20–30%, inflate debt (Germany exempts), and risk arms race spirals.

| Year | EU Avg % GDP | Total Spend (€B) | Key Driver |

| 2021 | 1.6 | ~300 | Pre-Ukraine |

| 2024 | 1.9 | 343 | Russia war |

| 2025 | 2.1 | 381 | Hague 5% pledge |

| 2035 Target | 3.5-5.0 | 1T+ extra | NATO core + security |

Overall, the following key points illustrate how the systemic risks of militarization threaten Europe's security more than they enhance it:

Doctrinal Shift: The militarization of the Eastern Flank80 is driven by a transition from "deterrence by punishment," trading space for time, to "forward deterrence"81 by denial. This strategy requires the "permanent stationing of substantial NATO forces" and a return to "military mass,"82 effectively converting the region from a political buffer into a fortified barrier. While this buildup of troops strengthens the physical defense of the Baltic states and Poland,83 it inherently escalates the security dilemma by placing combat-ready armored brigades directly on Russia's border,84 validating Russian narratives of encirclement.

The Input-Output Trap: A notable danger of swift militarization is the confusion between "input" (expenditure) and "output" (combat capabilities). Despite increasing resources, Europe remains significantly reliant on US assets, firepower, and military mass, such as Integrated Air and Missile Defense (IAMD) and intelligence capabilities.85 If European countries adopt a "wartime mindset," they risk militarizing their economies,86 which are known more for strong social safety nets than military strength, without achieving the strategic autonomy necessary for credible independent deterrence.87 This could happen if they cut back on social welfare funding and don't find a way to break the investment deadlock.

Erosion of Norms: Prioritizing "hard power"88 over diplomatic mechanisms like the CFE treaty runs the risk of an arms race. A NATO alliance that vastly outspends its adversaries may successfully deter aggression.89 Nevertheless, it also risks instigating an arms race that undermines diplomacy and established arms control norms. NATO leadership counters such claims by asserting that "weakness invites aggression"90 and that the present militarization is exclusively a defensive reaction to Russia’s total war economy. It may further strengthen Russia’s narrative of labeling NATO as an aggressive alliance91 and asserting that the permanent deployment of allied forces in the Baltics, Poland, Romania, and Bulgaria demonstrates that NATO's eastward expansion was intended to put an offensive wall to Russia and its former Soviet-era neighbors. This, coupled with Europe's peacetime security policy founded on arms control, transparency, and confidence-building mechanisms (CBMs),92 would render the concept worthless, notwithstanding its previous status as the cornerstone of European security.

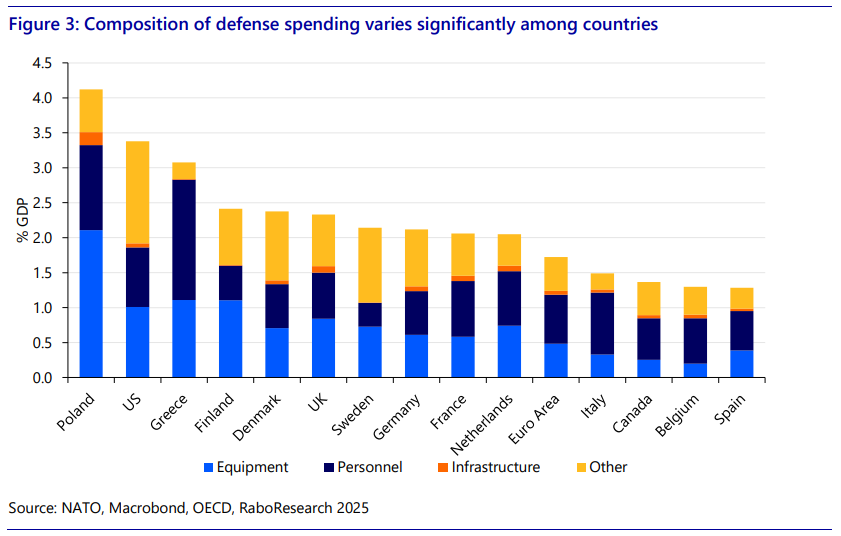

Fragmentation: Ultimately, the need for rearmament threatens to divide the alliance into a "multi-track NATO." As "star performers" in the East pursue aggressive militarization, "aspirational committers" and "laggards" in the West encounter internal political opposition to reducing social services for defense purposes.93 This fragmentation jeopardizes the collective cohesion essential for deterrence, where a strong frontline in the eastern flank will take up most of the military burden. More importantly, while the rearmament efforts manifest in increased defense spending and improved military capabilities, they also generate tensions and varied perspectives within NATO.94 Figure 10 showcases the different compositions of spending among European NATO members:

For Europe, currently, the primary criterion for enhanced deterrence continues to be financial and defense-related capabilities.

Defense as Deterrence

Europe stands at a historic golden moment to bolster its sovereignty and leverage NATO’s “defense as deterrence” posture. The convergence of an aggressive Russia, systemic rivalry from China, an uncertain American ally, and deep-seated internal fragmentation has created a perilous security environment. The surge in defense spending95 since 2022 signifies a necessary and profound break with the past, but it is only the first step on a long and difficult journey toward tackling traditional and non-traditional threats at its borders and beyond. Currently, the primary criterion for enhanced deterrence continues to be financial and defense-related capabilities. To translate financial commitments into a credible and sustainable defense posture, European leaders, through partnership in the NATO alliance, must confront four primary challenges.

- Overcoming the multi-track NATO: The "multi-track" nature of the alliance, where commitment and capability are highly imbalanced, is a strategic vulnerability. It heralds collective planning, hinders interoperability, and weakens the credibility of collective defense.96 A more equitable sharing of burdens and risks is paramount to NATO's ability to achieve its capability targets.

- Bridging the Capability Gap: Europe must move beyond simply increasing defense spending and focus on targeted investments to close its most critical shortfalls, especially in the technological sector.97 Priority must be given to acquiring capabilities essential for high-intensity warfare, such as integrated air and missile defense, long-range precision strike, and robust ISR assets, to establish a credible, independent deterrence.

- Developing the Industrial Base: Promoting the European defense industry98 is the prerequisite for military readiness and a key driver for the competitiveness of the European defense-equipment market. This requires governments to provide long-term demand certainty through multi-year contracts,99 which will give the industrial sector the confidence it needs to make necessary capital investments,100 demonstrate localization of production, secure supply chains, and overcome labor shortages.

- To reach true strategic alignment, the EU and NATO need to go beyond just being complementary. This means better coordinating their respective capability planning and procurement processes to avoid duplication, ensure interoperability, and maximize the efficiency of European defense investments.101 Cohesion policy, as illustrated in Defense Readiness 2030, already contributes to defense and security capabilities. It funds security and defense-related investments that contribute to regional development, as defense industries often create research and development and industrial ecosystems that benefit Europe’s regions and communities.

Collectively, we best understand the international implications of Europe's defense spending as structural rather than intentional.

Conclusions and Outlook

We cannot solely understand Europe's post-2022 surge in defense spending through the lens of regional deterrence or alliance burden-sharing. Rather, the surge reflects a deeper structural repositioning within an international system that is increasingly shaped by asymmetric competition among major powers. In this sense, Europe’s rearmament unfolds in the shadow of superpowers, most notably the United States, China, and Russia—whose strategic priorities, technological dominance, and industrial capacities constrain the range of autonomous choices available to European states.

From a strategic perspective, Europe does not emerge as an independent pole of military power through increased spending alone. Instead, defense investment represents a reactive adaptation to deteriorating external conditions: sustained Russian military aggression, China’s growing technological and industrial leverage, and uncertainty surrounding long-term US security guarantees. These pressures compel European states to enhance deterrence credibility while remaining embedded in alliance structures that limit full strategic autonomy. Defense spending, therefore, functions less as a pathway to independent power projection than as a mechanism for preserving relevance and reliability within an evolving alliance order.

This constrained positioning has broader international implications. First, Europe’s rearmament reinforces existing global power hierarchies rather than breaking them down. Despite increases in national defense budgets, European militaries remain structurally dependent on US enablers, including intelligence, surveillance, and reconnaissance (ISR), missile defense integration, strategic lift; and advanced command-and-control infrastructure. As a result, the expansion of European military capacity strengthens US-led deterrence and posture rather than producing an alternative center of strategic authority. In systemic terms, Europe’s defense spending stabilizes the Western security bloc while consolidating American centrality within it.

Europe’s increased military spending thus participates, though unintentionally, in the gradual hardening of the international security environment.

Second, Europe’s defense investments contribute to a broader normalization of militarized competition at the international level. The reallocation of fiscal resources toward defense-industrial expansion, munitions stockpiling, and high-technology military systems signals a shift away from the post-Cold War expectation that economic interdependence and institutional integration could substitute for hard-power preparedness. While this shift may enhance deterrence, it also accelerates the erosion of arms control regimes and confidence-building measures that historically mitigated escalation risks. Europe’s increased military spending thus participates, though unintentionally, in the gradual hardening of the international security environment.

Third, Europe’s rearmament generates spillover effects beyond the transatlantic space, particularly in global arms markets and technology diffusion. As European nations increase their purchases of missile defense systems, unmanned platforms, cyber capabilities, and military AI systems, they strengthen demand patterns that benefit established defense exporters and suppliers with cutting-edge technology. This dynamic strengthens concentration in global defense-industrial bases while limiting opportunities for smaller or non-aligned states to access comparable capabilities without deepening dependence on major powers. Consequently, Europe’s defense spending indirectly shapes global patterns of technological inequality and strategic alignment.

Historically, European actors have emphasized restraint, legal regulation, and multilateral governance in the use of force.

Finally, Europe’s defense surge complicates its normative positioning in international security governance. Historically, European actors have emphasized restraint, legal regulation, and multilateral governance in the use of force. Increased investment in high-tempo, technologically mediated military capabilities—particularly those associated with automation, AI-enabled command-and-control systems, and integrated missile defense—creates tension between Europe’s normative commitments and its material practices. Such investment does not imply normative abandonment but rather highlights a growing gap between governance aspirations and operational realities in a more contested international system.

Collectively, we best understand the international implications of Europe's defense spending as structural rather than intentional. Europe is adapting to systemic pressures that limit choice, shape dependency, and reinforce alliance-centric security architectures. In this context, defense spending enhances short-term deterrence and alliance credibility, but it also embeds Europe more deeply within a polarized global order defined by superpower competition. The long-term strategic challenge lies not in sustaining higher defense budgets per se, but in translating them into coherent capability development, institutional resilience, and governance frameworks that prevent rearmament from becoming an accelerant of systemic instability.

- Ferris, Layla. “How much do NATO members spend on defense? These are the countries that spend the most — and the least.” CBS News. June 25, 2025, Read More ↩︎

- Naishadham, Suman. “Spain rejects NATO's proposed defense spending increase as 'unreasonable.'” PBS News, June 19, 2025, Read More ↩︎

- NATO. “Defence expenditures and NATO’s 5% commitment.” NATO. December 18, 2025, Read More ↩︎

- European Commission. “White Paper for European Defence – Readiness 2030.” EU Commission, December 23, 2025, Read More ↩︎

- Arms Control Association. “The Conventional Armed Forces in Europe (CFE) Treaty and the Adapted CFE Treaty at a Glance.” ACA, November 2023, Read More ↩︎

- Stockholm International Peace Research Institute Research Report. “Confidence- and Security-Building Measures in the New Europe.” Oxford University Press, 2004, Read More ↩︎

- NATO. “To Prevent War, NATO Must Spend More, Speech by NATO Secretary General Mark Rutte at the Concert Noble, Brussels.” NATO, December 14, 2024, Read More ↩︎

- Mearsheimer, John J. The Tragedy of Great Power Politics. Updated ed. New York: W.W. Norton, 2014. Print.

↩︎ - John J. Mearsheimer, “Why the Ukraine Crisis Is the West’s Fault,” Foreign Affairs 93, no. 5 (September/October 2014): 77–89, Read More ↩︎

- Hall, Philip. ”John Mearsheimer’s Offensive Realism: In the Land of the Blind the One-Eyed Man is King.” Ars Notoria Magazine. August 20, 2025, Read More ↩︎

- Olson, Mancur, and Richard Zeckhauser. “An Economic Theory of Alliances.” The Review of Economics and Statistics 48, no. 3 (1966): 266–79. Read More. ↩︎

- Jervis, Robert. “Cooperation Under the Security Dilemma.” World Politics 30, no. 2 (1978): 167–214. Read More. ↩︎

- Ibid. ↩︎

- NATO Watch Committee, “Peace Research Perspectives on NATO 2030: A Response to the Official NATO Reflection Group,” February 2021, Read More ↩︎

- Siddi, Marco. 2022. “The Partnership That Failed: EU-Russia Relations and the War in Ukraine.” Journal of European Integration 44 (6): 893–98. Read More ↩︎

- European Commission News Article. “In Focus: Reducing the EU’s dependence on imported fossil fuels.” EU Commission, April 20, 2022, Read More ↩︎

- Kent, Laurent. “The US and Europe are still doing billions of dollars’ worth of business with Russia despite years of war.” CNN, August 28, 2025. Read More ↩︎

- EU Defense. ”COUNTERING HYBRID THREATS.” EU, March 2022, Read More ↩︎

- Jones, Seth. ”Russia’s Shadow War Against the West.” Center for Security and International Studies (CSIS). March 18, 2025, Read More ↩︎

- European Commission. “White Paper for European Defence – Readiness 2030.” EU Commission, December 23, 2025, Read More ↩︎

- Korda, Matt. ”The Pentagon’s (Slimmed Down) 2025 China Military Power Report.” Federation of American Scientists (FAS). January 9, 2026, Read More ↩︎

- Tohk, Tauno. ” More Than a Systemic Rival: China as a Security Challenge for the EU.” International Center for Defense and Security, Estonia. March 24, 2025, Read More ↩︎

- Hidayat, Muflih. ” Europe‘s Critical Rare Earth Challenge: Breaking China‘s Supply Dominance.“ Discovery Alert. November 1, 2025, Read More ↩︎

- Ibid. ↩︎

- Kalwasiński, Maciej and Bogusz, Michał. ” A blow dealt to Europe’s defence: China steps up control of strategic exports.” Center for Eastern Studies. October 14, 2025, Read More ↩︎

- Rostoum, Elly. ”Nexperia: China Puts Dutch in Check.” Center for European Policy Analysis. November 24, 2025, Read More ↩︎

- Hidayat, Muflih. ”China‘s Rare Earth Dominance Threatens Global Supply Chains Security.“ Discovery Alert. January 13, 2026. Read More ↩︎

- Szczepański, Marcin. ” China’s rare-earth export restrictions.” European Parliament. November 24, 2025, Read More ↩︎

- Hidayat, Muflih. ”China‘s Rare Earth Dominance Threatens Global Supply Chains Security.“ Discovery Alert. January 13, 2026. Read More ↩︎

- Oil, Gas & Energy Law. "China's Rare Earths Dominance and Policy Responses." Oxford Energy Institute, June 2023. Read More ↩︎

- Garcia-Herrero, Alicia. ”The EU, Russia, and China in a Changing Geopolitical Landscape.” Bruegel. March 31, 2025, Read More ↩︎

- MSN. ”Pentagon says China will have more than 1,000 nuclear warheads by 2030, posing direct threat to US.” MSN. January 2026, Read More ↩︎

- Gettleman, Jeffrey. ”Greenland Would Be the Largest U.S. Land Acquisition, if Trump Got His Way.” The New York Times. January 13, 2026. Read More ↩︎

- Rahn, Wesley. ”NATO talks Arctic security for Greenland amid US pressure.” DW. January 12, 2026, Read More ↩︎

- Chenghao, Sun. ”How China Reads the 2025 US National Security Strategy.” Brookings. January 12, 2026, Read More ↩︎

- Dysa, Yuliia. ” US offers 'free economic zone' in east if Ukraine cedes Donbas, Zelenskiy says.” Reuters. December 11, 2025, Read More ↩︎

- Bergmann, Max. ”Transatlantic Relations Under Trump: An Uneasy Peace.” CSIS. October 6, 2025, Read More ↩︎

- World Population Review. ” NATO Spending by Country 2026.” WPR. Read More ↩︎

- Ibid. ↩︎

- North Atlantic Treaty Organization, “Deterrence and Defence,” NATO Topics, updated December 10, 2025, Read More. ↩︎

- George C. Marshall European Center for Security Studies, “Strategically Speaking – Interview with SACEUR Commander General Cavoli,” podcast audio, April 22, 2024, Read More ↩︎

- Oneal, John R. “The Theory of Collective Action and Burden Sharing in NATO.” International Organization 44, no. 3 (1990): 379–402. Read More. ↩︎

- Cartmell, Rory. “Beyond the Billions: NATO's Defence Spending Pledges Mask a Multi-Track Europe,” King's College London, International Society, June 19, 2025, Read More ↩︎

- Ibid. ↩︎

- George C. Marshall European Center for Security Studies, “Strategically Speaking – Interview with SACEUR Commander General Cavoli,” podcast audio, April 22, 2024, Read More ↩︎

- Cartmell, Rory. “Beyond the Billions: NATO's Defence Spending Pledges Mask a Multi-Track Europe,” King's College London, International Society. ↩︎

- United24 Media. "Poland to Train 400,000 Citizens in ‘Largest Military Readiness Drive Since WWII.’" November 5, 2025. Read More ↩︎

- Sergi Pijuan and Elena Sánchez Nicolás, “The Turbo-Charging of EU Defence—Explained,” EUobserver, March 18, 2025, Read More ↩︎

- Heinemann, Noah. “Diverging Investments in European Defence: Germany’s and Sweden’s Policies towards NATO’s 2% Commitment.“ Atlantic Forum. November 1, 2025. Read More ↩︎

- rmy Recognition. "Germany Strengthens European Air Defense Capabilities With Israeli Arrow 3 Hypersonic Missile Interceptor." 2025. Read More ↩︎

- LAWLESS, JILL. "UK to Raise Defense Spending to 2.5% of GDP by 2027, Starmer Says." Associated Press, February 26, 2025. Read More ↩︎

- RFI. "Macron Seeks €36bn Boost in French Defence Spending by 2030." January 15, 2026. Read More ↩︎

- Daily Finland. "Sweden Announces Record Defense Budget Increase for 2026." October 28, 2025. Read More ↩︎

- Xinhua. "Finland Proposes Broad Spending Cuts in 2026 Budget, but Boosts Defense Funding." August 9, 2025. Read More ↩︎

- MIL3010. "Swedish Army, NATO. Archer Self-Propelled Howitzers during Military Exercises in Finland." Video, 7:20. YouTube. December 23, 2024.Read More ↩︎

- Nordefco. "Nordic Defence Cooperation Strengthens Regional Stability." Nordefco. January 19, 2026. Read More ↩︎

- Borsari, Federico and “Skip” Davis, Gordon B. "High Stakes in the High North: Harnessing Uncrewed Capabilities for Arctic Defense and Security." Center for European Policy Analysis (CEPA). December 2025, Read More ↩︎

- Natalizia, Gabriele, and Matteo Mazziotti di Celso. "Beyond NATO's 2 Percent Threshold: How Can Italy Meet the Challenge?" Atlantic Council, December 17, 2024. Read More ↩︎

- La Moncloa. "Spain Reaches Agreement with NATO to Allocate 2.1% of GDP to Defence." June 22, 2025. Read More. ↩︎

- Tian, Nan, Lorenzo Scarazzato, and Jade Guiberteau Ricard. "NATO's New Spending Target: Challenges and Risks Associated with a Political Signal." SIPRI Commentary, June 27, 2025. Read More ↩︎

- Hackett, James, et al. "Progress and Shortfalls in Europe's Defence: An Assessment—Introduction." International Institute for Strategic Studies (IISS), 2025. Read More ↩︎

- IISS and Defense Readiness 2030 data. ↩︎

- Hackett, James, et al. "Progress and Shortfalls in Europe's Defence: An Assessment—Introduction." International Institute for Strategic Studies (IISS). ↩︎

- European Central Bank. "How Vulnerable Is the Euro Area to Restrictions on Chinese Rare Earth Elements?" Economic Bulletin, Issue 6/2025. September 22, 2025. Read More ↩︎

- North Atlantic Treaty Organization. "NATO's Role in Capability Development." NATO. Last modified June 25, 2025. Read More ↩︎

- Beebe George , Episkopos Mark and Lieven Anatol. ”Right-Sizing the Russian Threat to Europe.” Quincy Institute for Responsible Statecraft. July 8, 2024. Read More ↩︎

- European Commission. "European Defence Fund." EU. January 19, 2026.Read More ↩︎

- Molle, Andrea. "Europe’s Defense Conundrum: Why PESCO and Other Initiatives Always Fall Short." STARTinsight, March 19, 2025. Read More ↩︎

- Council of the European Union. "European Peace Facility." January 19, 2026. Read More ↩︎

- Defense Readiness 2030. Footnote n.4. ↩︎

- European Commission. "SAFE | Security Action for Europe." Defence Industry and Space. May 29, 2025.Read More ↩︎

- Busch, Sarah. "Europe's Defence Dilemma: Rising Militarization Amidst Industrial Fragmentation and Weak Export Controls." PRIF BLOG, April 2, 2025. Read More ↩︎

- Eloranta, Jari. "Military Spending Patterns in History." EH.net Encyclopedia. Economic History Association, September 16, 2005. Read More ↩︎

- Andika, Reza, and Muhammad Erza Aimar. "The Security Dilemma and Arms Race Dynamics in Europe." Journal of Strategic and Global Studies 7, no. 2 (2024): 123-145. Read More ↩︎

- Clapp, Sebastian. "EU Member States' Defence Budgets." European Parliament Think Tank, May 7, 2025. Read More ↩︎

- Eloranta, Jari. "Military Spending Patterns in History." EH.net Encyclopedia. Economic History Association. ↩︎

- Ibid. ↩︎

- Ibid. ↩︎

- Erken, Hugo, Frank van Es, Elwin de Groot, and Lennart de Jong. "Europe in the New NATO Era." SUERF Policy Note 372 (July 2025). Read More ↩︎

- Niec, Piotr, and Benjamin, Jensen. "The Future of NATO's Eastern Flank." CSIS, International Security Program, Futures Lab, January 2026. Read More ↩︎

- Mälksoo, Maria. ”NATO's new front: deterrence moves eastward.“ Oxford University Press International Affairs Journal, Volume 100, Issue 2, March 2024, Pages 531–547, Read More ↩︎

- Pillai, Chad, and Kay Brinkmann. "Meeting Mass with Mass: Why NATO Matters to the U.S. Army." Military Review, November-December 2025. Read More

↩︎ - Kavanagh, Jennifer, and Jeremy Shapiro. "The Bear in the Baltics: Reassessing the Russian Threat in Estonia." European Council on Foreign Relations, December 2025. Read More ↩︎

- Gioe, David V., Marina Miron, and Marc Ozawa. 2025. “Reassessing NATO’s Deterrence and Defence Posture in the Baltics: Rebalancing Strategic Priorities to Counter Russian Hybrid Aggression.” Defense & Security Analysis 41 (1): Read More ↩︎

- Tanghe, Mila. "What European NATO Lacks." Interview with Maj. Gen. (rtd.) Gordon "Skip" Davis. CEPA Europe's Edge, March 2025. Read More ↩︎

- Bramlett, Virginia. "Rutte's 'Wartime Mindset' Sparks Debate Over Military vs. Social Spending." The Financial Analyst, December 15, 2024. Read More. ↩︎

- Kuang, Connie, Kary Bheemaiah, and Mylo Kidwell. "The Price of Security: Europe Is Set Up for a Serious Challenge." World Economic Forum, July 2025. Read More ↩︎

- Tian, Nan, Lorenzo Scarazzato, and Jade Guiberteau Ricard. "NATO's New Spending Target: Challenges and Risks Associated with a Political Signal." SIPRI Commentary, June 27, 2025. Read More ↩︎

- ibid. ↩︎

- Gheciu, Alexandra, and Stéfanie von Hlatky. "Irreconcilable Differences? NATO's Response to Russian Aggression Against Ukraine." International Journal: Canada's Journal of Global Policy Analysis 79, no. 2 (2024): 275–296. Read More ↩︎

- Westra, Lara. "Russia's Accusation of U.S. NATO Expansionism from 1989 to 2025: The Broken Promises Narrative Today." Atlas Institute for International Affairs, December 2025. Read More. ↩︎

- Arms Control Association. “The Conventional Armed Forces in Europe (CFE) Treaty and the Adapted CFE Treaty at a Glance.” ACA, November 2023, Read More ↩︎

- Cartmell, Rory. “Beyond the Billions: NATO's Defence Spending Pledges Mask a Multi-Track Europe.” King's College London, International Society, June 19, 2025, Read More ↩︎

- Van der Loo, Jorge. "Assessing the Impact of European Rearmament on NATO Relations." LinkedIn, April 9, 2025. Read More. ↩︎

- Defense Readiness 2030. ↩︎

- Cartmell, Rory. “Beyond the Billions: NATO's Defence Spending Pledges Mask a Multi-Track Europe.” ↩︎

- European Parliamentary Research Service. "ReArm Europe Plan/Readiness 2030." European Parliament, 2025.Read More ↩︎

- Ibid. ↩︎

- Defense Readiness 2030. ↩︎

- Speyside Group. "Rearming the Continent: NATO's Eastern Flank and the Future of European Security." Speyside Group. ↩︎

- European Parliamentary Research Service. ReArm Europe Plan/Readiness 2030. ↩︎

Content Type:Occasional Papers